Depreciation dilemma : Is it better to buy new or old properties?

Depreciation dilemma : Is it better to buy new or old properties?

When considering depreciation, which will gain the greatest benefit from capital allowances: new or old properties? That is the ongoing question – one that Paul Mazoletti from Napier & Blakeley aims to answer once and for all. Paul Mazoletti is a director at Napier & Blakeley, the first provider of depreciation schedules in the Australian market (since 1985).

When considering depreciation, which will gain the greatest benefit from capital allowances: new or old properties? That is the ongoing question – one that Paul Mazoletti from Napier & Blakeley aims to answer once and for all. Paul Mazoletti is a director at Napier & Blakeley, the first provider of depreciation schedules in the Australian market (since 1985).

Depreciation (capital allowances) can be a valuable tax deduction for any property investor and a great way to reduce your taxable income. However, the question of old versus new does come up a lot in discussions with investors. So, who is right and who is wrong? With effect from 9 May 2017, if you are focusing on capital allowances deductions, new property is the better way to go. We could also suggest that neither is the ‘best’ way, as there are advantages to both. However, if legislation is passed soon, the proposed changes will certainly lean you towards buying new.

The benefit of newer properties

The main benefit of buying a new investment property is that this will provide a higher total base tax deduction entitlement, when considering the combined value of fixtures and fittings the building structure’s value. Deductions through the depreciation of fixtures and fittings under Division 40 may now only be available on any new investment property asset acquisition made after 9 May 2017. Deductions through the depreciation of the building structure under Division 43 are also available on both new and older assets; we’ll explore this further later in the article. The ATO introduced capital allowances in 1985 for the residential sector, coincidentally at the same time as Napier & Blakeley opened its first office in Australia and launched its capital allowances business.

Since then, a few of the fundamentals of capital allowances have changed in regard to what you can claim on a property. What remains the same is the question of what provides the biggest deductions, and which properties provide the most value, particularly with regard to new and old properties. Every situation is different, and certainly newer properties are now looking very attractive, as outlined below. Deductions under ‘Capital Allowances’ are categorised into two main divisions:

- Division 43 Capital Works (Building)

- Division 40 Capital Allowances (Depreciating Assets – Plant)

Division 43 Capital Works (Building) – Old vs new

Division 43 relates to the calculation of the construction expenditure on both building and structural improvements. To calculate the construction expenditure for building allowance deductions as defined in Section 43-70 ITAA 1997, you require a suitably qualified person (a quantity surveyor) who can certify the cost of constructing a building, in addition to structural improvements such as driveways, fences, etc., as at the date they was installed and completed. This cost is then apportioned over the tax life of the building (usually 40 years or 2.5% per annum) and can be claimed as a tax deduction.

Second-hand residential deductions commence from when an investment asset was completed. For example, if in 2017 you purchased a 10-year-old house built in 2007, you need to determine the construction cost as at 2007 and start claiming an allowance per annum for the remaining 30 years, as 10 years have already passed. This is all you can claim now, in accordance with the proposed new legislation. If you recently purchased a new house, you have the next 40 years to claim this allowance per annum. The construction expenditure and size of the house will determine what you can claim in the year you buy or build, and how far into the future you can claim deductions is dependent on the age of the building. This also applies to low-rise townhouses and high-rise apartments.

Another consideration is that if the property is within a body corporate you will also be able to claim an additional portion of the building’s common property. This allowance depreciates the same as the building, but is apportioned in accordance with your interest entitlement. On a second-hand property you are allowed to claim any recent refurbishments and/or extensions as well. This can sometimes be attractive to buyers as they can claim for something old as well as new.

Example: If you purchased a large house built 10 years ago it may have cost $200,000 to build the structure and so you could claim this at 2.5% or $5,000 per annum for the next 30 years. If you purchased the same large new house today it may have a building structure cost of $300,000 and you could therefore claim at 2.5% or $7,500 per annum for the next 40 years. This is an example of how you can get more deductions for a new building than you do for an old building. If, however, you purchased the large house built 10 years ago and then refurbished/extended it, and these structural costs were an additional $100,000, then you could claim another 2.5%, or $2,500 per annum, for the new works for 40 years, plus the $5,000 for the next 30 years on the original structure. This would give you a total annual deduction of $7,500 per annum for at least 30 years.

Could items previously considered to be plant and equipment … now simply form part of the building and therefore become deductible as part of the building?

Rules of Depreciation

- Depreciation of fixtures and fittings under Division 40 is always available on any newinvestment property (to be confirmed by legislation shortly)

- You can generally claim 10–20% of a new property’s construction cost under Division 40

- For instance, a new property costing$400,000 to construct could generate $40k–$80k in capital allowance deductions over 10 years

- High-rise new apartments may attract more Division 40 deductions due to more communal amenities (eg lifts, pools)

If the property is within a body corporate, you will also be able to claim additional deductions from the building’s common property.

Division 40 Capital Allowances (Depreciating Assets – Plant)

Division 40 Capital Allowances (Depreciating Assets – Plant)

This part of the Act covers the principle of ‘decline in value’ of a depreciating asset. The definition of a depreciating asset is a separate topic that can’t be covered here. However, with the proposed new legislation as of 9 May 2017, Division 40 Capital Allowances (Depreciating Assets – Plant) are available only for the purchase of new properties, although at this stage we are not sure of the exact details until legislation is passed. But will this mean, for example, that items previously considered to be plant and equipment (and therefore deductible under Division 40) could now simply form part of the building and therefore become deductible as part of the building and included under Division 43 Capital Allowances deductions?

Some examples of depreciating assets are curtains, air conditioning, fire services, lifts, carpets, dishwashers and hot water units. The effective lives of these items were previously considered to be lower than the general building structure and therefore they could be depreciated more quickly, giving a higher write-off value per annum. The Australian Tax Handbook 2017, at 2,508 pages, lists all the capital allowances items you can claim and their respective effective lives. The ‘effective life’ determined by the ATO is its estimate of how long an item will last before it needs to be replaced, and this therefore determines the percentage depreciation rate. For instance, the effective life of curtains and drapes is six years, a ceiling fan lives for 20, an electric or gas hot water unit lasts 12 years and a solar hot water system lasts 15 years.

The cost base for depreciating assets was based on the principle of reasonable apportionment that is defined in Subdivision 40-195 of the ITAA 1997. The opening value of any depreciating asset is now the new purchase price and is not necessarily based on the age of the asset but on its income-producing capability and condition. This part of the Act will apply to all the depreciating assets of income producing buildings.

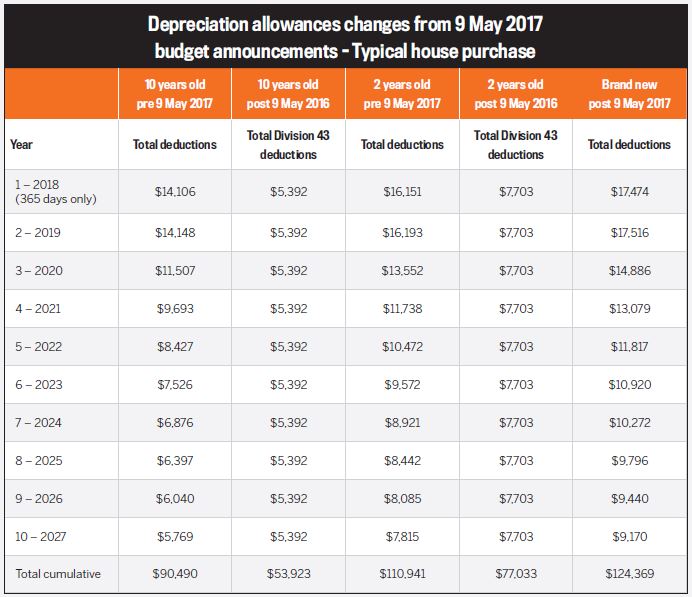

In simple terms, say a quantity surveyor inspects your property and determines that you have paid $2,000 for the curtains and drapes and these have an effective life of six years, the opening cost for depreciation will then be $2,000 and the taxpayer can claim an annual tax deduction of $333. There are as yet no details on how these plant and equipment items’ values will need to be treated during a taxpayer’s ownership, but they will likely have to be calculated the items’ written-down values at the time of purchase. There are also no details as to how costs for post 9 May renovations, refurbishments and extensions to investment assets will be treated or whether an investor can or cannot depreciate these items going forward. On a positive note, this may influence a boost in residential development as investors may be drawn to the higher deductions they can achieve by acquiring assets in new residential developments that are currently underway or planned for the future. In summary, new property may now have the greatest edge in terms of total deductions available, as shown in the table above.

Need help with depreciation?

Paul Mazoletti and the team at Napier & Blakeley have been helping Australian investors leverage depreciation schedules since 1985.

Ph. 07 3221 8255 www.napierblakeley.com

We have prepared depreciation schedules for all kinds of investors and properties, both residential and non-residential, for over 30 years and there are always so many variations to consider when constructing your depreciation schedule. There are many factors to consider when determining this, which is why investors should use a quantity surveyor. Keep in mind that professional fees to engage a suitable quantity surveyor are 100% deductible and will ensure your deductions are calculated accurately and in accordance with current legislation.

Published in Your Investment Property

August 2017