Capital Allowances: Draft Effective Lives of Assets used in Transfer Stations and Landfill Services

Capital Allowances: Draft Effective Lives of Assets used in Transfer Stations and Landfill Services

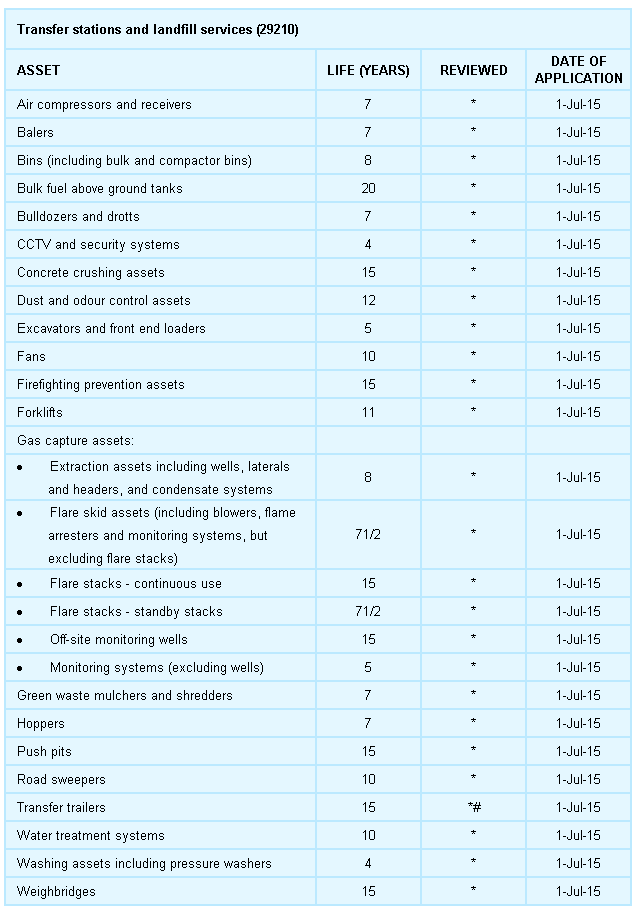

The following is a recent release from the ATO and their understanding of new Effective Lives which can now be used for depreciation purposes, effective from July 2015 for the Transfer Station and Landfill industry sectors.

They are seeking comments on a draft list of Effective Lives they are releasing for assets used in Transfer Stations and Landfill services.

Proposed new determinations

They are proposing to add the following list of Effective Life determinations to the Commissioner’s schedule to apply to new assets either purchased and first used, or installed ready to use, on or after 1 July 2015 (within the meaning of section 40-95 of the Income Tax Assessment Act 1997). The effective life listed below for each asset basically determines the depreciation rate e.g.: 20 life years = a basic rate of 5% per annum can be claimed on the cost of the item to the income producing taxpayer.

CAPITAL ALLOWANCES UPDATE: TR 2013/4 New effective lives of depreciable assets – Applicable from July 1 2013

If you enjoy keeping up to date with the tax laws, the following will interest you! This new ruling and determination is issued as part of an ongoing review of the Commissioner’s effective life determinations. Taxpayers use ‘effective lives’ to work out how much they can claim as a tax deduction for an asset’s decline in value (depreciation deduction).

The Commissioner has made a determination of the effective life of certain depreciating assets. This will take effect from 1 July 2013. If you have your property or business in the following ANZIC categories this will affect reporting on your new purchases after July 1 2013 of Division 40 Plant/Assets.

Industries and industry activities affected are:

Industries and industry activities affected are:

- Ammonia and ammonium nitrate manufacturing (fertiliser, dyes, herbicides)

- Meat processing (beef, pig & sheep abattoirs – not chicken)

- “Non-ferrous metal casting (aluminium)

- Pet food manufacturing (canned, bird feed, cereal for fodder, sheep lick)

- Prefabricated concrete manufacturing (precast walls, panels)

- Sanitary paper product manufacturing (toilet paper, tissues, napkins)

Determinations made by The Commissioner for the effective life and depreciation assets, has been applied for the purpose of provisions under division 40, which will be effective in the life of depreciating assets. This will be used to work out the assets decline in value. Continue reading